The Securities and Exchange Board of India on Tuesday ushered in key changes to its index derivatives framework, in a bid to curb wild speculation, especially among retail investors. The six changes, which differ partially from the proposals mooted in the earlier consultation paper, will be rolled out in phases from November 20.

The contract size for index derivatives has been raised to ₹15-20 lakh from ₹5-10 lakh currently. The earlier consultation paper had suggested a phase-wise increase in contract size up to ₹30 lakh.

“Given the inherent leverage and higher risk in derivatives, this recalibration in minimum contract size, in tune with the growth of the market, would ensure that an inbuilt suitability and appropriateness criteria for participants is maintained as intended,” the regulator said in its circular. .

“Increasing F&O contract size could significantly inhibit small traders in Nifty and Bank Nifty due to a minimum 100 per cent increase in margin requirements. Additional 2 per cent ELM margin on expiry day will restrict expiry day option sellers. The regulator seems to be concerned about this zero-dated options trading because of which calendar spread benefit is removed on expiry day,” said Tejas Khoday, CEO of FYERS.

-

Also read: SEBI set to curb booming options frenzy as risks abound

Derivative contracts

Each exchange will now be able to provide derivative contracts for only one of its benchmark indices with weekly expiry. Different stock exchanges offer short tenure options contracts on indices which expire on every day of the week. The SEBI consultation paper had noted that there is hyperactive trading in index options on expiry day, with average position holding periods in minutes, accompanied by increased volatility in the value of the index through the day and at expiry.

Both the above measures will be effective from November 20.

The benefit of offsetting positions across different expiries referred to as ‘calendar spread’ will not be available on the day of expiry for contracts expiring on that day. This will align calendar spread treatment with cross-margin framework on correlated indices having different expiries, wherein such cross-margin benefit is fully revoked at the start of the first of the expiring correlated indices.

In a bid to avoid undue intraday leverage and discourage allowing positions beyond the collateral at the end-client level, the regulator has mandated collection of options premium upfront from option buyers. The upfront margin collection requirement will include net options premium payable at the client level. The same may be included in the intraday snapshots conducted by clearing corporations and for imposition of penalty for non-compliance.

Both the above norms will become applicable from February 1, 2025.

The existing position limits for equity index derivatives will be monitored intra-day by exchanges, instead of end-of-day, from April 1. For this purpose, stock exchanges will consider minimum four position snapshots during the day, randomly taken during pre- defined time windows.

-

Also read: Nation of Gamblers. F&O Trading and The Great Indian Slaughterhouse

short options

An additional extreme loss margin (ELM) of 2 per cent will be levied for short options contracts from November 20. This would be applicable for all open short options at the start of the day, as well on short options contracts initiated during the day that are due for expiry on that day.

The regulator has not rationalized the strike price introduction methodology that was proposed in the consultation paper.

The six changes are based on the suggestions made by a SEBI-appointed expert working group and subsequent deliberations by the secondary market advisory committee.

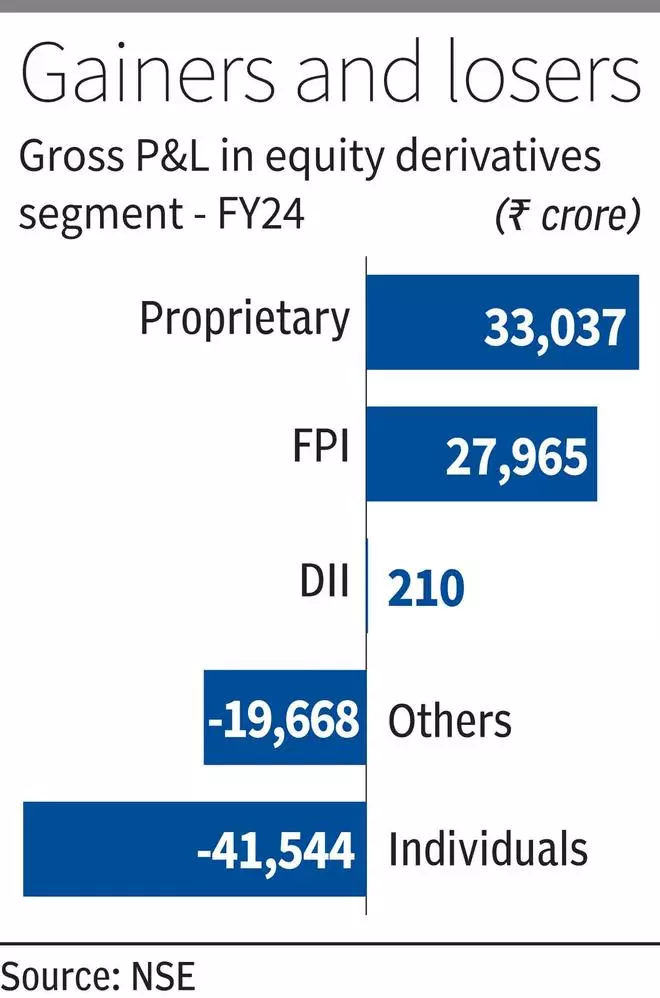

A recent SEBI study had revealed that aggregate losses of individual traders exceeded ₹1.8 lakh crore between FY22 and FY24. Ninety three per cent of over 1 crore individual F&O traders incurred average losses of around ₹2 lakh per trader, inclusive of transaction costs.